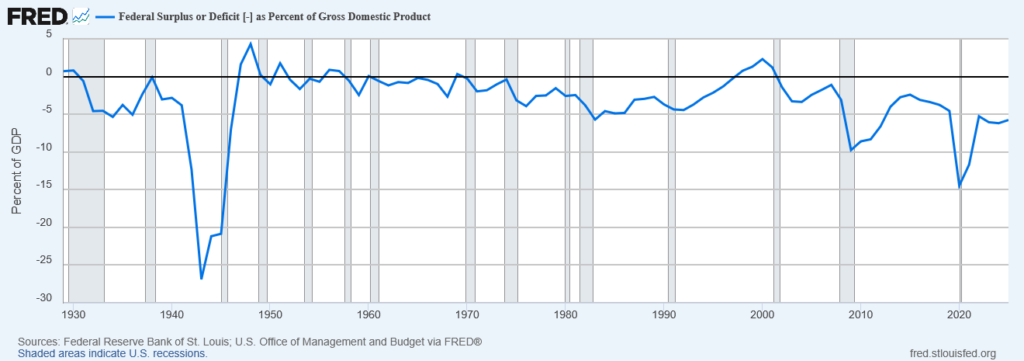

The trajectory of the US Government’s deficit spending is a real concern. To illustrate, here is a chart showing the deficit as a % of GDP throughout time:

As you can see, from the end of World War II until the early 1980’s the US spending deficit was generally range bound between 0%-5% of GDP. During the Reagan/Bush years, the deficit increased slightly due to tax cuts. The Clinton Administration and a Republican-controlled Congress got their act together and realized a rare surplus – with much help from a roaring economy and the dot com build-up. However, the dot com crash, 9/11, the Great Financial Crisis, and the COVID pandemic have induced a deterioration in the fiscal health of the United States over the past 25 years.

The last data point from the graph above is from 2025, with the deficit at ~5.8% of GDP. It’s likely (but not guaranteed) to trend higher in the coming years as the OBBBA comes into full effect in over the rest of 2026.

This level of deficit spending unsustainable. Warren Buffett, among other bright minds, has indicated that a sustainable amount of deficit spending is around 3% of GDP. At this level, the US dollar should remain in good standing around the world, even with the massive existing federal debt burden. But sustained deficit spending of 5-6% will eventually create problems. At a certain point, an out of control deficit will feed on itself as the annual debt service payments grow. Much like a snowball rolling down hill, gobbling up a larger and larger portion of the overall spending budget. If we can get to 3% of GDP, that would be fantastic!

What we need is some rational thinking in DC. Unfortunately, rationality is in short supply at the moment. The current administration believes that we can accelerate GDP growth and enact tariffs to increase revenue and bring the deficit down. However, a large and sustained increase in GDP growth is unlikely to happen without a major paradigm shift in the US and global economy. Perhaps the large promises around artificial intelligence can get us there, but it’s hard to see that happening at this point. And as far as tariffs go, they are simply a national sales tax. They should help with the deficit a bit, but likely not to the extent envisioned by policymakers.

And speaking of taxes, even staunch historical defenders of tax cuts are starting to see the writing on the wall. The truth is that it will likely take a combination of meaningful spending reductions and tax increases to rein in the deficit. And the sooner the better. The longer that Congress dithers, the harsher future changes will become. Unfortunately, Congress is unlikely to take meaningful action anytime soon.

The good news is that Congress’s hand will likely be forced at some point in the future, we just don’t know when. We also don’t know what the exact catalyst will be, but whatever it is will likely blow a hole in market demand for US Government debt. At that point, simple microeconomics and supply/demand will take over. Less demand will drive bond offering prices down. And as prices decrease, interest rates will increase, perhaps in a big way.

What does this mean from an investment perspective?

Unfortunately, the size and scope of the US Treasury market is such that it will be awfully difficult for many investors to steer around a deficit-fueled debt crisis in the US. The simple answer is “avoid owning US debt.” However, even if you move into other areas such as corporate debt, you really won’t be all that safe. A default by the US Treasury would likely ripple through corporate balance sheets and cause a significant crisis in corporate debt prices as well.

One likely outcome of an out-of-control federal deficit is higher inflation. Inflation is, after all, one of the main tools that policymakers can use to rein in the deficit in real terms. So how do we handle the possibility of higher future inflation?

Real assets such as gold, commodities, or real estate likely could offer some protection. Gold has historically demonstrated an uncanny ability to keep up with inflation – over long periods of time. But remember, that we can only really expect gold to match future inflation, not surpass it. After all, gold doesn’t produce or create anything of value. It is simply a store of value. For real returns (or returns above inflation) we’ll have to look elsewhere.

“Elsewhere” in this case likely means stocks. As economic engines that produce valuable goods and services and provide significant innovation and improvement over time, the companies in the stock market offer significant potential to provide meaningful real returns and beat inflation over time. Will it be a smooth ride? Certainly not. If the US Treasury defaults or the market loses faith in the US Treasury markets, stocks could fall precipitously. But over time, it’s likely that stocks will recover as the markets adapt. International stocks could also offer a good hedge against a debt crisis in the US.

What other things should we consider?

Alongside higher inflation, it’s likely that interest rates will move higher to compensate bond holders for the additional risks associated with the federal deficit. Higher interest rates mean lower bond prices, so any retiree using bonds as a reserve fund for future living expenses may consider looking at ways to shorten overall duration and interest rate exposure. I likely wouldn’t recommend that a retiree own a large amount of 30-year US Treasury bonds. It may be a good idea to consider using short-term bonds to manage cash flow needs over the next 3-5 years.

On the plus side, many retirees have low debt burdens (i.e. their house is paid off, cars are paid off, etc.) so higher interest rates likely won’t create large additional costs. In fact, many retirees actually have a lower personal inflation rate than what the CPI indicates in large part because they often own their home so aren’t subject to inflation on the “rent” component of living expenses.

In addition to a higher baseline of inflation, it’s also possible that Congress will need to boost federal tax revenues to reduce the deficit. This means higher tax rates in the future. Higher taxes could mean a combination of higher income tax rates, tariffs, or even an newly created value-added tax (VAT). It’s hard to what will happen at this point. But it’s unlikely that US tax rates will increase anytime soon as both Republicans and Democrats are indicating a preference for cutting taxes for most of the middle class. However, all else equal, Roth conversions are likely more attractive if tax rates increase down the road (with the caveat that lots of variables come into play with Roth conversions).

Social Security benefits could also see a reduction or cut in the future. I’m skeptical that Congress would allow an across-the-board benefit cut, but anything is possible. More likely I think is that Congress will seek to preserve benefits for older folks and reduce benefits mainly for younger people (say age 50 and under). Do I have any definitive proof for this assertion? Not really. It just seems more likely to me at this point, but I could be wrong.

What’s the urgency here?

Do I think the US debt markets are in immediate danger? Not at all. In fact, US debt markets remain quite robust for one really good reason… there is simply no viable alternative to US Treasuries in the global financial markets at this time. Many countries are diversifying their currency reserves by buying gold or other foreign currencies (e.g. Swiss Francs, Chinese Yuan, etc.), but none of these offer the same level of market depth and liquidity as the US Treasury market, so Treasury auctions continue to be well subscribed. There is simply no alternative. It may not the best argument in favor of owning US debt, but I suppose it could be worse.

The truth is, nobody really knows when or if an deficit-fueled debt crisis will materialize. The deficit math has been concerning for a while and has certainly become more alarming ever since COVID, but I don’t believe that we’ve reached the point of no return. Congress certainly could figure out a solution if they had the political will to do so. Let’s hope that they do figure it out as soon as possible.