As we approach mid-year, I thought it might be useful to offer some reflections about the markets.

1 – Beating the Market is still hard (insanely hard)

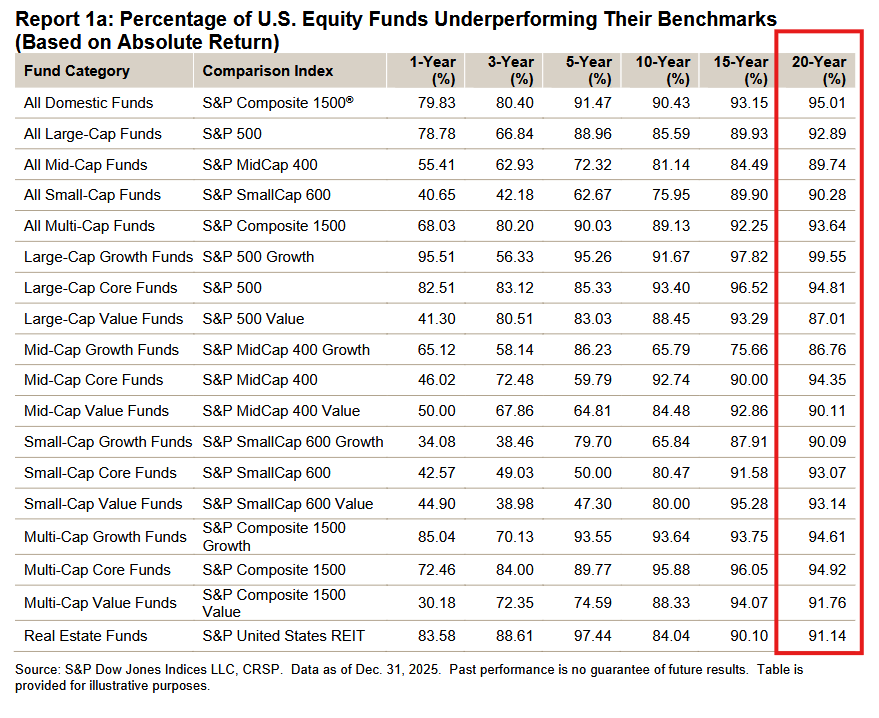

If you are not familiar with the SPIVA scorecard, it’s a good reference to examine how actively managed investment funds compare to a set of standardized passive benchmarks. Here is the data for US equity funds as of 12/31/2025 (note the column in red):

The reality is, over long periods of time, about 90% of active managers will underperform a reasonable passive benchmark. Some flavors of US equity funds have slightly better or worse results than others, but that 90% level is a good reference point. And this applies both on an absolute basis (e.g. just comparing raw returns) and on a risk-adjusted basis (e.g. comparing returns adjusted for volatility). And if you’re interested in how much they underperform, the aggregate amount of underperformance is very likely close to the aggregate fees charged by the funds. Sharpe made this argument a long time ago with simple arithmetic.

And these results aren’t confined to US stock funds, or even stock funds in general. Both international stock funds and bond funds show similar results (you can see for yourself by looking at all of the tables at the end of this report).

The important thing to remember is that even someone who knows nothing about stocks or investing can expect to outperform 90% of the most highly educated and intelligent people on the planet simply by buying a low-cost, passive index fund.

2 – Stock returns have been great, but it’s important to manage expectations

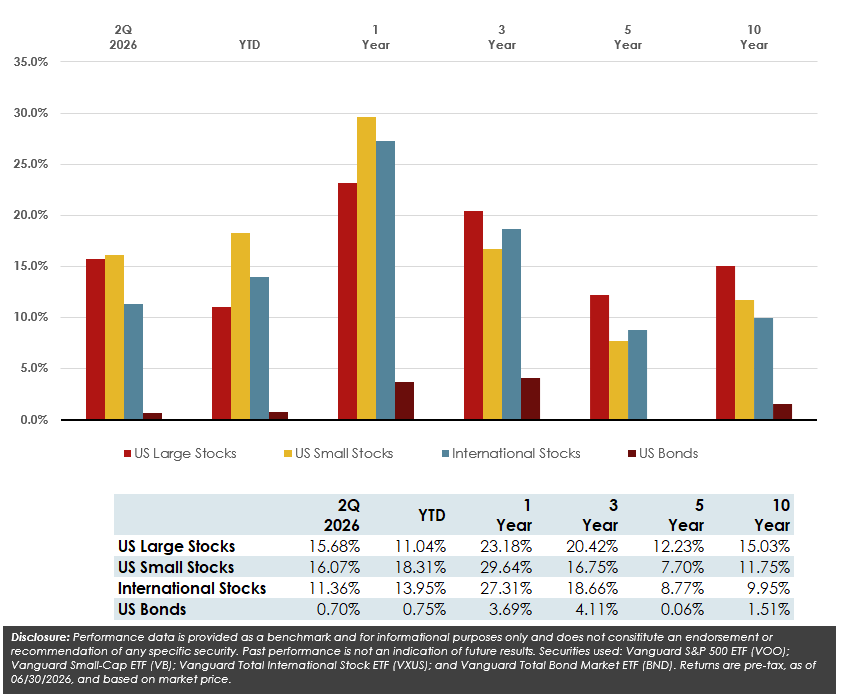

Stock market returns in the second quarter were phenomenal! It’s hard to imagine, but over the past 10 years, large US stocks have returned 15% per year! Even international stocks have returned 10% per year! If you had invested $1 in US/International stocks 10 years ago, that same dollar is worth about $4.05 or $2.58 today (respectively, ignoring taxes).

And keep in mind that this all happened in the face of innumerable economic and geopolitical concerns. The war in Iran this past spring, widespread tariffs last year, a near banking crisis from Silicon Valley Bank in 2023, the invasion of Ukraine in 2022, high levels of inflation and economic concerns coming out of COVID in 2021-2022, the onset of COVID in 2020, trade war concerns at the end of 2018, increased political and cultural angst, etc.

I think this is a good example of the power of long-term investing. The ride may not always be smooth or friendly, but if we stick with it, we can likely expect a good result!

However, I think it’s important to manage our expectations. When it comes to investing, I like the saying “you play the game going forward” when it comes to investing. And on that note, I think it’s unlikely that the next 10 years of stock returns will be in line with the past 10 years, but of course I could be wrong. If you are creating a financial or investment plan today, it might be prudent to reduce your return expectations a bit. If we end up getting 15%/year over the next 10 years, that will be great! But I just don’t think it’s likely.

3 – Interest rates likely aren’t coming down anytime soon

At the start of the year, it appeared that the Federal Reserve was on track to reduce short-term interest rates in line with lower inflation expectations. But with the onset of the war in Iran, inflation numbers have jumped up a good amount. Now the markets are expecting 2-3 rate increases in the near future. If you were waiting for mortgage rates to come down a bit before refinancing, it’s likely you’ll have to wait a good bit longer.

4 – US stock returns are more widespread this year

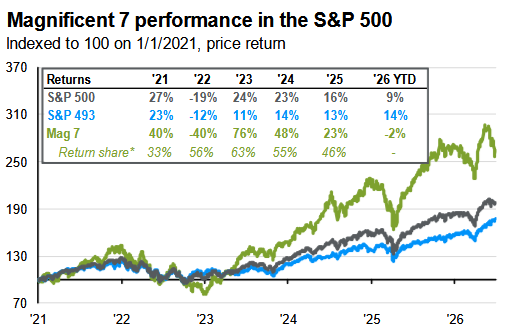

Many investors have been concerned about increased concentration within the S&P 500. The so-called Magnificent 7 (or Mag 7), which includes Apple, Amazon, Google, Meta/Facebook, Microsoft, Nvidia, and Tesla have produced about 45-50% of the returns for the entire S&P 500 over the past 5 years, but so far in 2026 the other 493 companies have picked up some slack:

And for those worried about concentration, I think it’s important to remember that the Mag 7 represent a large portion of the total S&P 500 for a good reason… they earn a lot of money for investors! And so far, they have demonstrated an great ability to grow their earnings over time. The Mag 7 may not be on top forever, but right now, it’s hard to argue why they shouldn’t be.

5 – Artificial Intelligence (AI) continues to dominate

If the performance of the S&P 500 has been more broad based in 2026, then where are those returns coming from? Generally from other, smaller tech companies! 32 of the top 50 performers in the S&P 500 so far this year are tech companies. More specifically, companies with exposure to the insatiable demand of AI companies.

For example, the top performer so far this year is SanDisk. They make computer components that are useful in data centers.

The second best performer is Micron. They also make computer components that are useful in data centers.

The third best performer is Western Digital. They also make computer components that are useful in data centers.

I’m sure you see the pattern here. Essentially all of the top 10 make computer components useful for AI companies.

6 – I’m still not a big fan of gold

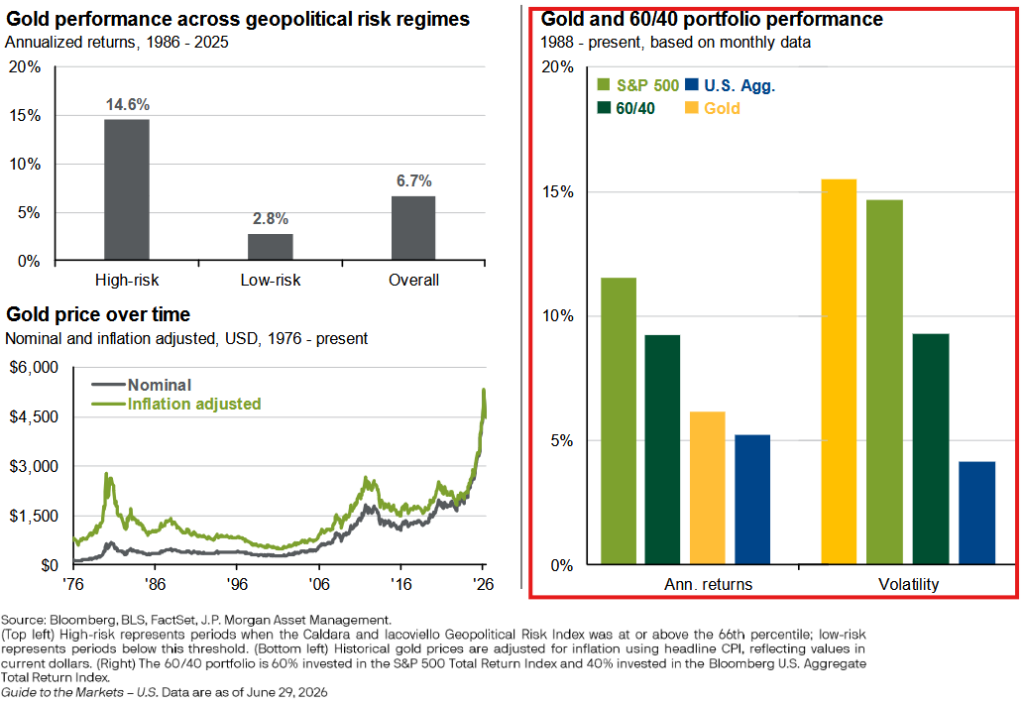

The price of gold has skyrocketed over the past few years, likely in response to higher than average inflation in the post-COVID period and heightened geopolitical concerns both in the US and around the world.

To be clear, I’m fine with most investors owning a small amount of gold in their portfolio as it could offer some diversification benefits, but I’m just not a huge fan of gold’s long-term investment potential. Here is a chart showing why:

Over the past 38 years, gold has underperformed both the S&P 500 and a 60/40 equity/bond portfolio. And it has done so with a tremendous amount of volatility. So more risk and less reward… not exactly a winning combo.

Based on this, I have two thoughts.

1) If you can stomach the volatility of owning gold, then you might as well own stocks instead!

2) If you prefer to reduce the volatility of your portfolio (which many retirees find reasonable and essential), then you might as well own something like a 60/40 portfolio… based on history you could still outperform gold, just with less ups and downs.

At the end of the day, my belief is that the best we can hope for from gold is to keep up with inflation over long periods of time. For example, going back to Ancient Rome, the price of a loaf of bread is more or less the same as it is today when priced in gold. So gold has certainly delivered on thousands of years of inflation protection.

But gold doesn’t generate any earnings or new technology or new business processes or innovations. It simply sits there. A store of value? Definitely (if you can handle the bumpy ride). A source of long-term wealth generation and “real” returns? I just don’t see it.

If you have questions or disagreements, please let me know. Thanks for reading!