The short answer is not really. Here’s why:

#1 – Any proposed allocation would be tiny

Take a look at this article by Morningstar. In the last paragraph, Arnott points out that global private equity assets totaled about $11 trillion and the public equity markets totaled about $115 trillion. So the combination of private + public is about $126 trillion. Private equity represents 8.7% of the total. So if you are a passive investor and want to replicate the entire global stock market (private + public), then you would allocate 91.3% of your stock allocation to public equities and the other 8.7% to private equities.

Most people – especially retirees – don’t hold 100% stocks. What about a portfolio comprised of 50% stocks and 50% bonds? Then your theoretical allocation for private equity should be about 0.5 x 8.7% = 4.3% of your portfolio.

In the grand scheme of things, a 4% allocation won’t really make much of a difference. In fact, a 4% allocation for almost anything won’t really move the needle all that much. For example, if you are trying to decide whether you should own 50% stocks or 54% stocks, just flip a coin and be done with it. When it comes to asset allocation, I always recommend thinking in chunks of 10%. Anything less really isn’t worth the time or effort.

And this all assumes that you actually want to allocate a full share to private equity. As Arnott points out in the article, many investors will be scared off by the high fees and liquidity constraints of private equity funds, which could induce an investor to underweight their PE allocation. I have seen this play out quite often reviewing portfolios for potential new clients. If they have PE funds (or really any private investment), then it’s generally a pittance or token allocation. Often, just enough to offer the illusion of a more clever portfolio. But in practice, the portfolio would likely perform just the same (if not better) by removing the private equity allocation.

If you aren’t going to make a meaningful allocation to private equity, then you’ll likely be better off not making any allocation at all.

#2 – You’ll end up playing with the B-team or worse

The work of money managers, like most work produced in life, is 90% crap. This applies to PE fund managers as well. The biggest and best private equity firms (i.e. the top 10%), will almost always get the best deal flow with the best terms. These firms can also attract the best or most skilled investment professionals. All of this enables the top tier firms to generate the lion’s share of returns and out-performance (with much of that “alpha” flowing to the fund managers themselves).

Unfortunately for all of us regular folks, top tier PE funds are in high demand and mostly only take new capital from large institutional investors (think pension funds, university endowments, or billionaires). They won’t take your money unless you can write a check for $100 million. Let’s call these top tier firms the A-team.

The 2nd tier of private equity managers (let’s call them the B-team), are smaller or regional firms. Perhaps they have some reasonable competitive advantages such as an effective niche market or a talented founder or CEO. They may deliver some positive results, but likely not with the scale or consistency of the top tier firms. And they are going to be the second call for many companies looking to transact. That first call is going to the A-team firms.

We’ll call everyone else the C-team. These are the under-performers. They may have good marketing and sales practices which help them gather investor capital, and they may benefit from a positive market environment. After all, it’s easy to make money when the market is trending up. This can paper over any problems for a good long while. But eventually, results will demonstrate that these firms don’t have any true skill or competitive advantage in the marketplace. Clients of C-team firms would almost certainly be better off by simply owning a passive index fund.

Now what if I said that there are about 19,000 private equity funds in the US? What do you think your chances are of picking one of the few fund managers that has real skill and will generate good results? Remember, you can’t access the A-team, they are booked up. You’re forced to pick a B-team fund manager (or worse). Good luck.

#3 – Private Equity is really just leveraged small-cap exposure

Verdad Capital has made a convincing case that private equity investing is akin to buying small-cap companies, but using a lot of debt (or leverage) to do so. This makes intuitive sense, because this pretty much describes exactly what private equity funds are doing everyday. These funds are going out into the market and buying up small(er) companies and structuring the deals such that they put minimal amounts of their own capital at risk. Most of the capital used to make investments comes from the target company taking on significant debt.

Private equity companies likely do have some advantages over a leveraged small-cap strategy. This is mainly in the form of effective financial engineering and access to low cost debt capital. But even consumers these days have methods for accessing low-cost borrowing if they want to try to replicate PE returns leveraged small-cap investments.

#4 – The fees are very high

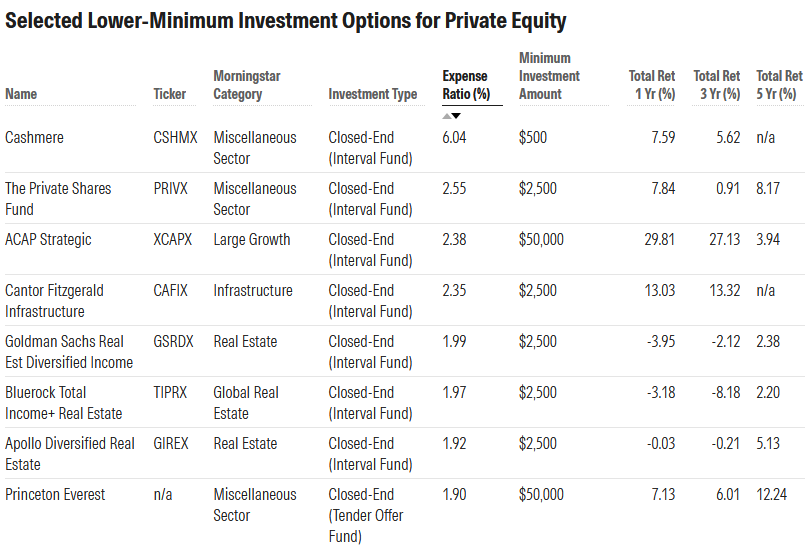

Here is a screenshot from the Morningstar article listing some retail private equity fund options. These are generally B and C tier PE funds – remember that A tier funds won’t take your money. Note the fees.

I’m going to ignore the Cashmere fund as an outlier. The remaining funds have an average annual fee around 2%. This means that a low-cost, passive index fund has a 2% head start each year. That’s like being in pretty good shape and running 5K race with a 5 or 10-minute head start. The elite runners (A-team) may be able to catch you. But the B and C-team folks will struggle to do so.

#5 – PE funds often engage in volatility “laundering”

One thing that attracts many investors to PE funds is the notion that they are less volatile than their publicly traded counterparts. This is a fallacy however. There’s no magic rule that says the value of a private company will fluctuate less than a public one. If two identical companies existed, and one was public and one was private, their intrinsic value and market prices should move in lockstep.

To lessen visible volatility, PE funds simply update their pricing less often and/or don’t fully adjust the values of portfolio holdings to reflect market conditions (i.e. during a stock market crash). This is known as volatility laundering and it gives PE funds the veneer of higher risk-adjusted returns (i.e. same or better return with less volatility).

And from the point of common sense, since PE funds mainly invest in small companies, and have less diversification than a passive index fund, there should be more volatility, not less.

Unfortunately, volatility laundering is not a bug, but rather a feature when it comes to the private investing ecosystem. Many PE fund investors are quite aware that the volatility is being laundered, and they are generally ok with it. After all, if your run a university endowment and your PE fund managers are artificially suppressing volatility, then it makes your risk-adjusted returns look better. You can then use this data in your annual performance report and argue for a bigger bonus. Many people in the institutional investing space stand to benefit from volatility laundering, this includes financial advisors that incorporate PE funds in client portfolios. As Charlie Munger used to say, “Show me the incentive and I’ll show you the outcome.”

Thanks for reading!